Online banking has made managing money easier than ever. With just a smartphone or laptop, you can transfer money, pay bills, check balances, and even apply for loans within minutes. Banks advertise online banking as fast, free, and convenient. But here’s the truth many customers discover later — online banking is not always as free as it seems.

Behind the convenience, there are several hidden fees and charges that banks rarely highlight in advertisements. These small charges may look insignificant at first, but over time they can quietly drain money from your account.

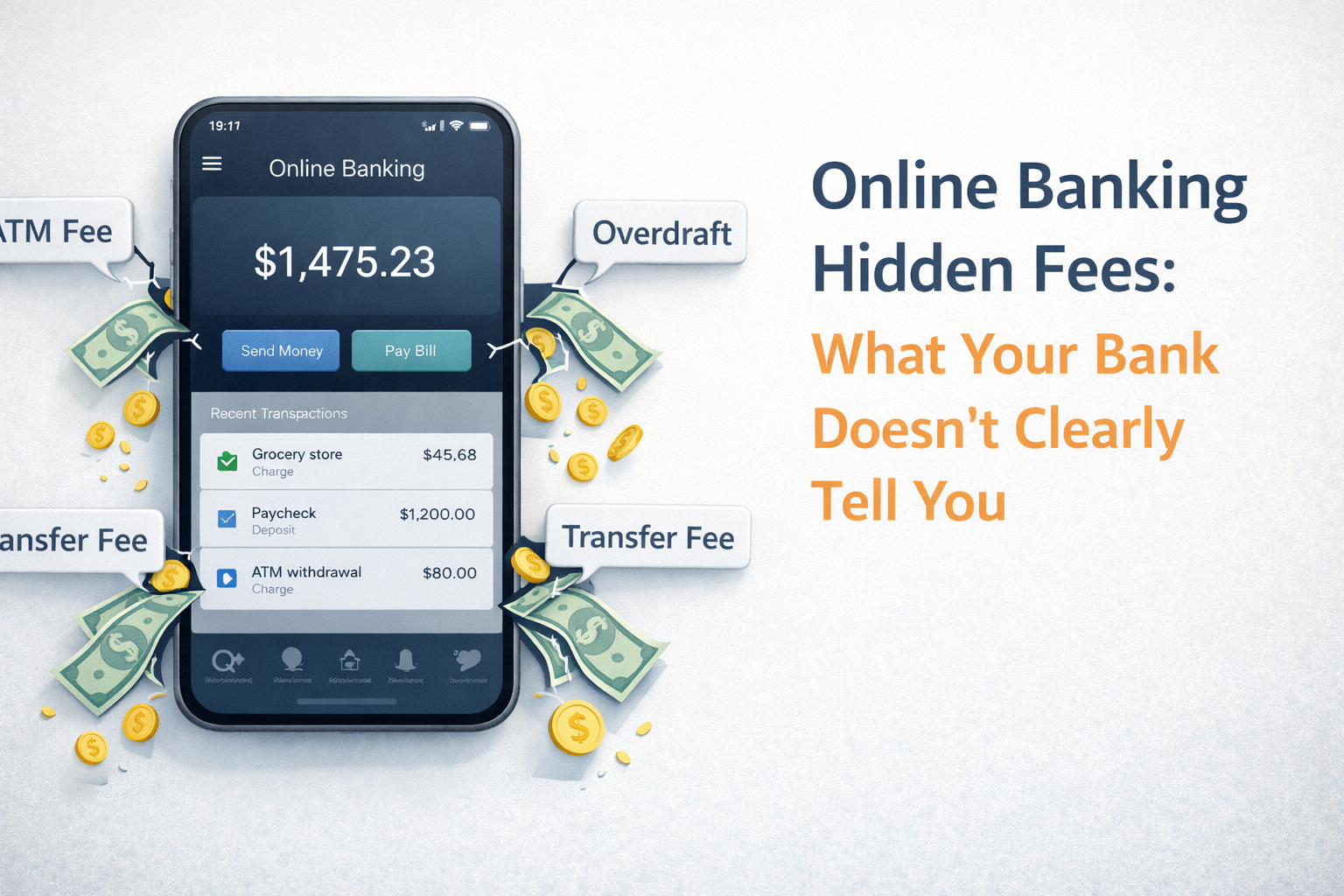

In this article, we’ll uncover the hidden fees in online banking that banks don’t clearly tell you about, so you can protect your money and avoid unnecessary charges.

Why Banks Promote “Free” Online Banking

Banks promote online banking heavily because it reduces their operational costs. When customers use apps or websites instead of visiting branches, banks need fewer employees and physical locations.

To attract users, banks often advertise services like:

- Free online transfers

- Free account management

- Zero maintenance fees

- Instant payments

However, the word “free” usually comes with conditions. Many charges are hidden inside the bank’s fee structure or terms and conditions — documents most people never read.

1. Monthly Maintenance Fees

One of the most common hidden fees in online banking is the monthly maintenance fee.

Some banks charge a monthly fee just for keeping your account active. Sometimes it’s labeled as:

- Account maintenance fee

- Digital service fee

- Platform usage fee

In many cases, banks waive this fee only if you maintain a minimum balance. If your balance drops below that amount, the bank automatically deducts the fee.

For example:

- Minimum balance required: $1,000

- Monthly maintenance fee: $5 – $15

Many users don’t notice these deductions until months later.

2. ATM Withdrawal Fees

Online banks often claim to offer free ATM withdrawals, but that’s not always true.

You might face two types of ATM fees:

- ATM operator fee – charged by the ATM provider

- Bank withdrawal fee – charged by your bank

If the ATM is outside your bank’s network, you could pay both fees.

For example:

- ATM operator fee: $3

- Bank fee: $2.50

That’s $5.50 for a single withdrawal.

If you withdraw cash multiple times per month, these fees can add up quickly.

3. Transfer Fees for Certain Transactions

Online banking usually allows free transfers between accounts in the same bank. However, not all transfers are free.

Some transactions that may involve hidden fees include:

- Instant transfers

- International transfers

- Transfers to external banks

- Real-time payment systems

For instance, sending money internationally may include:

- Transfer fee

- Currency conversion fee

- Hidden exchange rate markup

Banks sometimes advertise low transfer fees, but the real cost is hidden in the exchange rate.

4. Overdraft Fees

Overdraft fees are one of the most expensive hidden charges in banking.

An overdraft happens when you spend more money than what is available in your account. The bank temporarily covers the difference — but charges a fee for doing so.

Typical overdraft fees range from:

- $25 to $35 per transaction

Imagine this situation:

- Your account balance: $10

- You make a payment of $30

Your bank may approve the transaction but charge a $35 overdraft fee, meaning you now owe $55 instead of $20.

Many users don’t realize they have overdraft protection enabled until they see these charges.

5. Inactivity Fees

Some banks charge inactivity fees if you don’t use your account for a certain period.

If there are no transactions for 6–12 months, the bank may start deducting a monthly fee.

For example:

- Inactivity fee: $5 – $10 per month

This is common for accounts people forget about, such as old savings accounts or secondary online bank accounts.

6. Foreign Transaction Fees

If you use your online bank card internationally or make purchases in another currency, you may be charged a foreign transaction fee.

This fee usually ranges between:

- 2% – 3% of the transaction amount

For example:

- Purchase amount: $200

- Foreign transaction fee (3%): $6

While $6 might seem small, frequent international transactions can significantly increase your expenses.

7. Paper Statement and Service Fees

Even in digital banking, some services still cost money.

Banks may charge extra for:

- Paper statements

- Replacement debit cards

- Customer support services

- Expedited transfers

For example:

- Paper statement fee: $2 – $5 per month

- Card replacement fee: $10 – $20

These charges are often buried in the bank’s fee schedule.

How to Avoid Hidden Online Banking Fees

The good news is that most hidden banking fees can be avoided with a few simple steps.

1. Always Read the Fee Schedule

Every bank publishes a fee schedule document. It lists all possible charges associated with your account.

2. Maintain Minimum Balance

If your account requires a minimum balance, make sure you maintain it to avoid monthly fees.

3. Use In-Network ATMs

Withdraw cash only from ATMs within your bank’s network.

4. Turn Off Overdraft Protection

If possible, disable overdraft protection to avoid expensive overdraft fees.

5. Monitor Your Transactions

Regularly check your account activity to detect unexpected charges early.

The Bottom Line

Online banking is incredibly convenient, but it’s not always completely free. Hidden fees like maintenance charges, ATM fees, overdraft penalties, and foreign transaction costs can slowly reduce your savings if you’re not paying attention.

Banks rely on the fact that most customers don’t read the fine print.

The smartest approach is simple:

Understand your bank’s fee structure before opening an account.

By staying informed and monitoring your transactions regularly, you can enjoy the benefits of online banking without paying unnecessary hidden fees.